EDITOR'S NOTE: Paul Krugman is a New York Times columnist and is Distinguished Professor at the City University of New York Graduate Center. He won the 2008 Nobel Memorial Prize in Economic Sciences for his work on international trade and economic geography.

Other WRAL Top Stories

Friday’s consumer price report came as a huge surprise to almost everyone — because the numbers came in almost exactly in line with expectations, which basically never happens. Analysts whose job is to forecast what official numbers will say a few hours before they come out — a job of dubious usefulness, but whatever — expected the one-year rate of inflation to come in at 6.8%; it came in at ... 6.8%. “Core” inflation, which strips out volatile food and energy prices, came in right on expectations too.

If there was any information content in Friday’s release, it was that extreme scenarios in both directions became a bit less likely. There wasn’t anything in the report suggesting that inflation is rapidly spiraling upward; nor was there anything lending comfort to those hoping to see inflation fade away in the next few months.

For what it’s worth, financial markets appear to have taken onboard the reduction in risks of really high inflation: “Breakeven rates,” which measure market expectations of the inflation rate over the next few years, came down modestly. But nothing major happened.

That said, the headline number is highly likely to come down over the next few months, if only because the big run-up of oil prices from their pandemic lows seems to have gone into reverse.

Oil wells that end well? Bloomberg

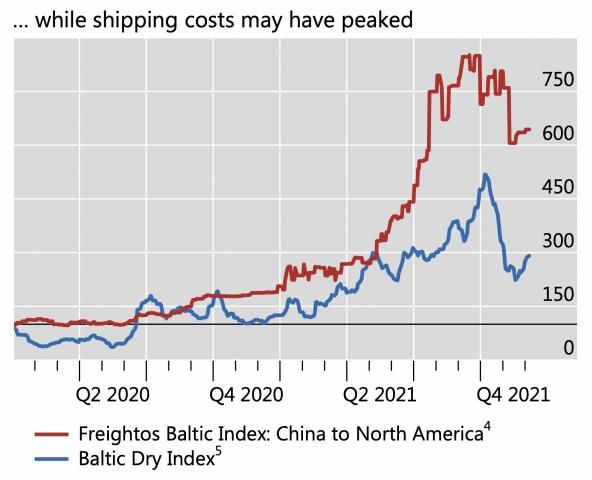

Some other components may also be coming down — or will at least stop rising rapidly. Hyun Song Shin, head of research for the influential Bank for International Settlements, recently made the case that a lot of recent inflation reflects the “bullwhip effect”: panic or at least precautionary buying of goods that seem to be in short supply, which intensifies the shortage. (Remember last year’s toilet paper shortage?)

Shin points out, among other things, that shipping costs, while still very high, seem to have peaked.

Containers contained? Bank for International Settlements

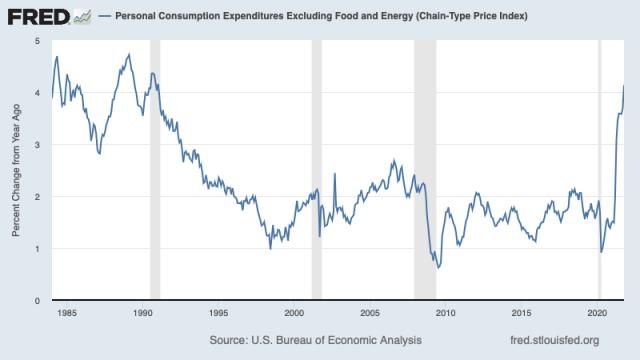

But even if you try to adjust for special circumstances, underlying inflation appears to be running high by recent standards, maybe around 4% instead of the 2% that is the Federal Reserve’s target and has been the norm since the mid-1990s. This in turn reflects an economy in which spending is more or less back to the pre-pandemic trend but production is constrained both by bottlenecks and by the withdrawal of several million Americans from the labor force.

As an aside, 4% inflation isn’t hyperinflation; it isn’t even the double-digit inflation of the 1970s. In fact, whether they know it or not, Americans of a certain age can attest that it’s not so bad. It was, after all, the inflation rate that prevailed for much of the Reagan years — you know, after morning in America.

Those horrible 1980s. FRED

I, at least, don’t remember the late 1980s as hellish.

Still, the Fed would consider a sustained doubling of the inflation rate a blow to its credibility. So how long will elevated inflation last?

The secret answer (don’t tell anyone) is that we don’t know.

I still think the most likely scenario is a minor league version of the 1946-48 inflation spike, when pent-up demand after the end of wartime rationing caused an inflationary boom — inflation peaked at around 20% — but price stability quickly and more or less painlessly reemerged once the spending surge was over. I still don’t see any evidence that 1970s-type stagflation, in which everyone kept raising prices because they expected everyone else to keep raising prices, is emerging.

But Friday’s numbers neither reinforced nor challenged my beliefs. This report was shockingly unsurprising.

This article originally appeared in The New York Times.