That's right -- the interest can be even higher than your credit cards.Credit counselors say it's fine to take advantage of no payments till nextyear. Just be sure check the fine print and pay it off before the heavyinterest kicks in.

We've all seen the ads. So what does consumer credit counselor Wayne Freeman think of them?

"The first thing I think is, 'What a deal!' But, look at the fine printtosee whether or not it is a deal."

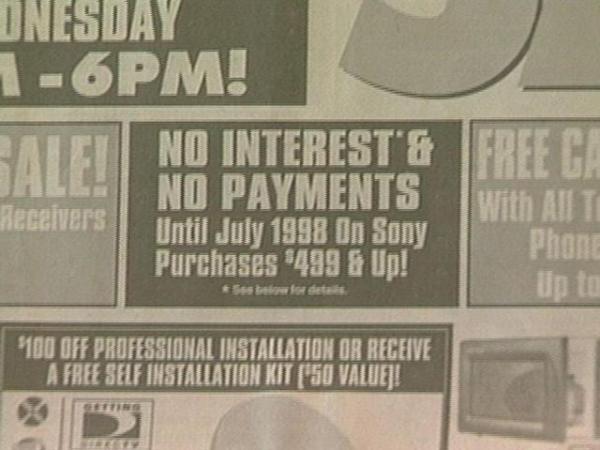

For instance, Herbert Battle bought a Sony Trinitron Wednesday morning atCircuit City. He paid cash, but the store's circular says he couldfinanceit with no payments and no interest until July.But, if you don't pay every penny by July, you'll be charged interest allthe way back to the date of purchase.

Counselor Wayne Freeman says the key is knowing yourself, your financesand your deal.

"If I thought I could pay for it within the promotion's period, then, yes, it's a good deal."

Typically, these promotions focus on big ticketitems, like furniture, cars, appliances, or electronics. But, when theinterest starts, watch out. It can be more than 20 percent.

The bottom line: Whether these deals save you money depends on one thing-- whether you paythe balance on time.

Credit Counselor Wayne Freeman also advises that you always ask for adisclosure statement with the cash price, credit price, interest rate andterms of the agreement. Retailers are required to provide it but you maynot get it unless you ask.

Copyright 2024 by Capitol Broadcasting Company. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

for 2024 season")